Due Diligence in Dental Practice Acquisitions: What to Expect

Table of Contents

- 1 What Due Diligence Means in a Dental Practice Sale

- 2 What Buyers Usually Review During Due Diligence

- 3 Confirmatory vs. Investigatory Due Diligence

- 4 What Builds Confidence During Due Diligence

- 5 What Creates Friction and Starts Weakening the Deal

- 6 How to Recognize When Due Diligence Is Going Off Track

- 7 What Sellers Most Often Misunderstand

- 8 How Preparation Before Diligence Changes the Outcome

- 9 Why Due Diligence Matters to the Outcome of the Deal

Due diligence is one of the most important phases of a dental practice sale, but it is also one of the most commonly misunderstood.

From the seller's side, it can look like a flood of document requests, follow-up questions, and additional review after the buyer has already made an offer. That is why some owners assume due diligence is mostly administrative. In practice, it is more important than that. It is the stage where the buyer validates whether the practice performs the way it was presented earlier in the process.

Due diligence determines whether the records, reports, and operational details support the story that brought the deal this far. Before diligence, the buyer may review production reports, hear explanations about cash flow, and discuss growth opportunities. During diligence, that same buyer begins verifying production, collections, payroll, expenses, patient flow, and the records supporting the transaction. In other words, the process shifts from evaluation to validation.

When the assumptions behind the deal hold up, confidence usually grows, and the transaction moves forward more smoothly. When they do not, timelines can slow, more questions can follow, and the deal can become harder to close under the original expectations.

What Due Diligence Means in a Dental Practice Sale

Due diligence typically begins after the buyer and seller sign a Letter of Intent. At that point, the transaction moves beyond early interest and into a deeper review of the practice.

The purpose of due diligence is to help the buyer gain access to more detailed financial, operational, and practice-level information to confirm that the practice performs as represented and that the assumptions supporting the proposed transaction are backed by the facts.

That makes due diligence different from the earlier buyer review that happens before the LOI. Early review helps a buyer decide whether a practice is worth pursuing. Due diligence begins once the buyer decides the opportunity is worth validating in detail.

In many dental practice transactions, the buyer's diligence rights may remain active through closing, even if the bulk of the review happens earlier. That is partly because dental acquisitions involve a meaningful amount of goodwill, transition risk, and patient-retention questions that cannot be fully evaluated through a few summary reports alone.

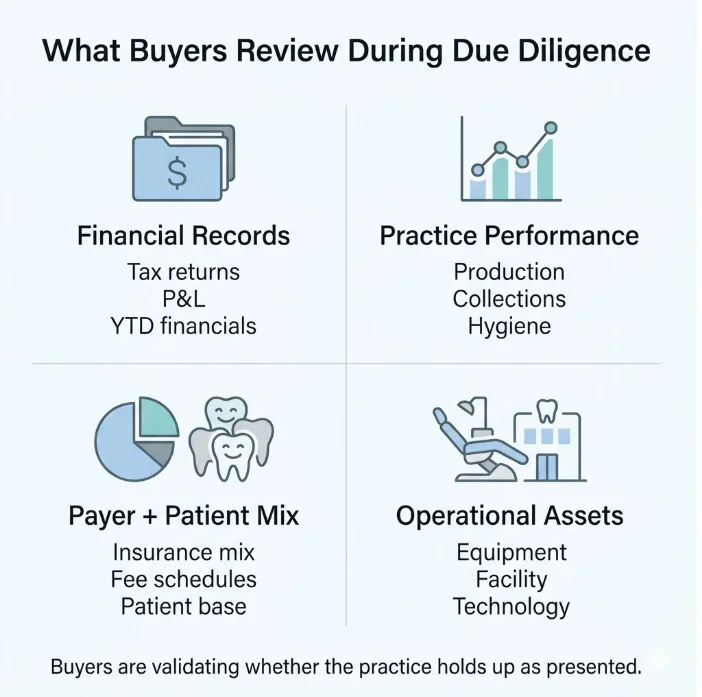

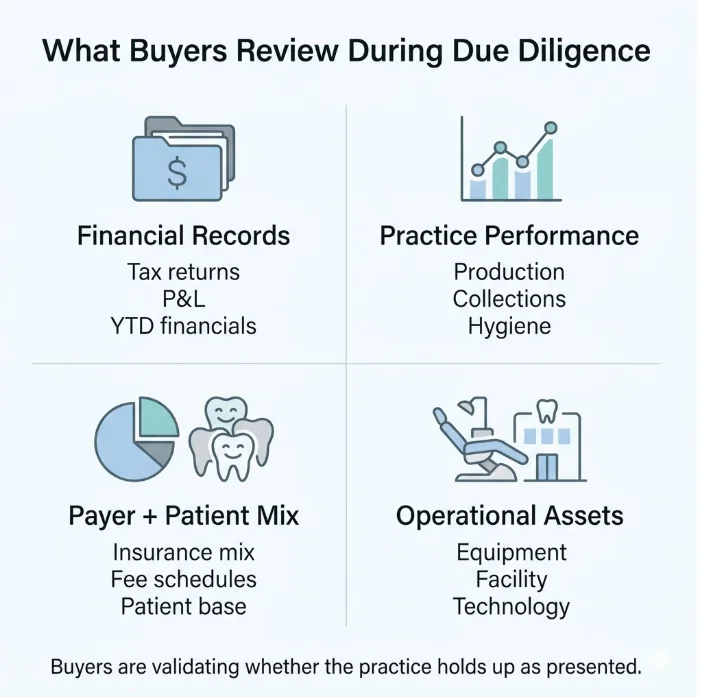

What Buyers Usually Review During Due Diligence

While due diligence can feel like a collection of endless checklists from the seller's side, most buyers are trying to understand whether the practice holds up from the inside once the source information becomes available.

At a high level, buyers usually review four broad categories of information.

1 Financial Records

This often includes tax returns, profit and loss statements, balance sheets, and current year-to-date financials. Buyers want to confirm that the revenue, expenses, profitability, and cash flow assumptions used earlier in the process are supported by the underlying records. Most buyers are not looking for perfect numbers. They are looking for consistency.

2 Practice Performance Reporting

This can include production by provider, collections, hygiene performance, procedure mix, referral patterns, and other reports generated from the practice management system. These reports help buyers understand how the practice actually operates day to day, how dependent it is on the owner, and how well the opportunity aligns with their clinical goals and long-term plans.

3 Payer and Patient Information

Buyers often want to understand the mix of fee-for-service, PPO, Medicaid, and other insurance participation, along with the fee schedules and revenue dependence tied to those plans. This helps them evaluate reimbursement quality, patient demographics, and how the practice fits their intended operating strategy.

4 Operational and Physical Assets

This usually includes an additional practice visit, facility review, equipment review, and a closer look at technology and day-to-day systems. In some cases, buyers or their advisors may also review information directly in the practice management software or perform limited chart review to better understand documentation and operational consistency.

Across all four categories, the buyer's goal is the same: to determine whether the practice performs the way it was presented and whether the information supports the assumptions behind the proposed deal.

Confirmatory vs. Investigatory Due Diligence

One of the most useful ways to understand due diligence is to distinguish between confirmatory diligence and investigatory diligence.

In a confirmatory diligence process, the buyer is mostly verifying what was already represented earlier in the transaction. The tax returns align with the financial story. The practice reports support the production and collections figures. The operational reality of the practice generally matches expectations. Questions still arise, but they are usually aimed at understanding details rather than resolving concerns.

In an investigatory diligence process, the buyer is no longer just confirming assumptions. The information starts creating new questions. Records may be incomplete. Reports may cover different periods. Explanations may not fully reconcile what the documents show. In that environment, the buyer shifts from validation into investigation.

That shift does not automatically mean anyone has done anything wrong. It often means the information is harder to understand, slower to obtain, or less consistent than expected. But it still changes the tone of the process. Instead of each new document reinforcing confidence, each new document is being used to answer a question created by the last one.

The type of due diligence affects pace, confidence, and momentum. A confirmatory process tends to move the transaction toward closing. An investigatory process tends to make the path slower and less predictable.

What Builds Confidence During Due Diligence

The strongest confidence-building signals during diligence are consistency, organization, transparency, responsiveness, and clear explanations.

Consistency is usually the most important. Buyers become more comfortable when financial statements, tax returns, practice reports, and operational details all support the same story. The issue is not whether every practice is flawless. The issue is whether the information holds together in a way that makes the business understandable.

Organization matters because it changes the quality of the review. When documents are current, accessible, and easy to interpret, buyers spend less time trying to reconcile the information and more time validating the opportunity. An organized diligence process often signals that the practice itself has been managed in a disciplined way.

Transparency matters because known issues are usually easier to work through than issues that appear late in the process. Most buyers understand that every practice has strengths, limits, and areas for improvement. A clear explanation early on often creates less concern than something the buyer discovers after assumptions have already formed.

Responsiveness matters for a similar reason. Buyers do not expect a seller to respond instantly while still running a practice. But timely answers help keep the process focused on confirmation rather than uncertainty. Questions arise in every transaction. The smoother the flow of information, the easier it is for confidence to build.

Confidence also tends to build when the process feels coordinated rather than reactive. When buyers can get the information they need, understand what they are reviewing, and move from one diligence question to the next without repeated gaps, the transaction starts feeling more stable. That helps buyers, advisors, and lenders, where relevant, keep moving toward the same goal instead of spending more time trying to resolve avoidable uncertainty.

For sellers, that is an important mindset shift. A well-run diligence process is not only about avoiding problems. It is also a chance to reinforce that the practice has been represented accurately, managed thoughtfully, and prepared for a serious transition.

When these elements are present, due diligence moves from being a compliance exercise to becoming an opportunity for the seller to reinforce the value of the practice and help the transaction keep moving in the right direction.

What Creates Friction and Starts Weakening the Deal

Friction during diligence usually begins when buyers cannot quickly understand, verify, or reconcile what they are reviewing.

Sometimes the cause is obvious, such as missing records or inconsistent reports. Other times it is more subtle. A practice may have strong performance overall, but if key reports cover different time periods, supporting documents are difficult to locate, or explanations come only after several rounds of follow-up, the review process becomes slower and more complicated.

Another common source of friction is when the assumptions formed earlier in the transaction do not fully match what diligence reveals. That can relate to provider production, staffing arrangements, payer participation, equipment needs, referral patterns, or transition expectations. Many of these issues are manageable, but they still require more analysis before the transaction can move forward confidently.

In most cases, friction during diligence does not come from one dramatic discovery but from small uncertainties that start accumulating faster than they are being resolved.

When that happens, the most common consequence is not an immediate collapsed deal. More often, the process slows down. Buyers ask more follow-up questions. Additional support may be requested. Discussions around price, transition structure, or financing may become more complicated if the information no longer supports the original assumptions as clearly as expected.

How to Recognize When Due Diligence Is Starting to Go Off Track

Not every follow-up question is a warning sign. A normal diligence process includes clarifying questions about finances, operations, staffing, production, and other parts of the practice. If the buyer asks a question, gets a clear answer, and moves on, that is usually a healthy sign.

The process may be starting to go off track when the buyer returns to the same issue repeatedly, asks for multiple documents to answer one original question, or keeps seeking additional support after explanations have already been provided.

Another useful signal is the purpose of the questions. In a normal process, the questions are helping the buyer understand the practice. In a strained process, the questions are aimed at deciding which facts can be relied upon and which still need further investigation.

Once the conversation shifts from understanding the practice to testing the reliability of the information itself, the transaction can become slower, heavier, and more difficult to keep on track.

What Sellers Most Often Misunderstand About Due Diligence

One of the most common seller misconceptions is that due diligence is mainly testing whether the practice is good. In reality, it is usually testing whether the practice matches the buyer's understanding of it.

That's an important difference. Most buyers are not expecting perfection. They know every practice has strengths, challenges, and areas that could be improved. What they need to know is whether the information they relied on when deciding to pursue the opportunity accurately reflects reality.

Another common misconception is that strong performance can compensate for weak records. It often cannot. A practice may produce very well, but if the buyer struggles to verify the numbers or reconcile what is being presented, uncertainty can still develop.

Sellers also sometimes assume buyers are only checking finances. In reality, buyers are evaluating the full picture. They are looking at production patterns, payroll, payer mix, equipment condition, operational consistency, and how transferable the practice will be after the transition.

One more misconception is that the LOI effectively settles the deal. It does not. The LOI creates the framework for the transaction, but due diligence is still where the assumptions behind that framework get tested against the records and the practice itself.

How Preparation Before Diligence Changes the Outcome

The most helpful preparation before diligence begins is not creating an oversized data room for every possible scenario. It is making sure the information buyers are most likely to request is organized, current, and accessible. That is one reason a practice can attract interest and still not be fully sale-ready.

That usually starts with the basics: tax returns, financial statements, and current year-to-date reporting. It also includes being able to generate common practice management reports without unnecessary delay and being prepared to explain how the records connect to the story that was presented earlier.

Preparation changes the process because it changes how easily the buyer can validate the practice. When the information is ready and understandable, diligence tends to remain confirmatory. When the seller is still trying to gather and reconcile basic records after diligence has already started, the buyer spends more time figuring out the information than validating the opportunity.

Reactive preparation creates more risk than many sellers realize. It slows momentum, creates avoidable uncertainty, and can make the practice feel harder to evaluate than it should. In some cases, buyers who are still deciding where to focus their time may shift their attention toward opportunities that are easier to diligence and move forward with.

Why Due Diligence Matters to the Outcome of the Deal

Due diligence is one of the last major points in the transaction where the practice has to hold up under deeper review. It is the phase where the buyer moves beyond summaries and assumptions and begins confirming whether the business actually supports the story that brought the deal this far.

When the records, reports, and explanations consistently support that story, the process tends to move forward with confidence. When they do not, the transaction can become slower, less predictable, and more difficult to close.

The lender dimension is part of this as well. In many transactions, the buyer's diligence process and the lender's underwriting process are moving at the same time, often using many of the same financial and operational records. When the information is organized, consistent, and easy to provide, both processes tend to move smoothly. When questions remain unresolved or supporting documentation is difficult to obtain, the buyer's financing process can slow down along with the diligence process. That is also why deal structure can become more complicated once diligence and underwriting start testing the original assumptions more closely.

Due diligence is not designed to create problems. It is designed to validate the opportunity. Buyers are not usually looking for perfection. They are looking for confidence that the practice performs as represented and that the information supporting the transaction is accurate, understandable, and timely.

When that standard is met, diligence becomes a stage where the value of the practice can be reinforced, and the transaction can keep moving toward a successful closing.

Get your practice ready before diligence begins

A free valuation gives you a clear picture of where your practice stands so you can enter the process with confidence.

Value Your Practice

About the Author

Andrea Berk is an entrepreneur and business strategist specializing in dental practice growth, operations, and practice transitions. She is the Founder of The Dental Shop, where she works closely with dentists at every stage of their careers to help them make smarter decisions around buying, selling, scaling, and optimizing their practices. Andrea brings a practical, real-world perspective to complex business challenges facing dental professionals today. Her work focuses on helping practice owners increase efficiency, improve profitability, and build long-term enterprise value—without losing sight of patient care or work-life balance. Andrea regularly publishes insights on dental practice management, business strategy for dentists, practice transitions, and entrepreneurship, offering actionable guidance designed to help owners navigate growth with clarity and confidence. When she’s not advising practice owners, Andrea is focused on building scalable systems and partnerships that elevate independent dental practices nationwide.