Why Deal Structure Matters More Than Most Dental Practice Owners Realize

Table of Contents

- 1 Why A High Offer Is Not The Same As A Financeable Deal

- 2 What Lenders Are Actually Underwriting

- 3 Why Financing Structure Changes What A Buyer Can Actually Pay

- 4 What Makes A Deal More Or Less Bankable

- 5 How Sellers Misread Financing Strength

- 6 The Real Question Sellers Should Ask About Deal Structure

Many dental practice owners think they have a deal once a buyer is enthusiastic, the parties agree on price, and a letter of intent is signed. That is understandable. At that point, the transaction feels real.

In dental practice sales, what feels real early in the process is not always what proves real under financing scrutiny. A deal can look strong in conversation and still weaken once financing is tested. Price can be agreed. Buyers can be serious. Momentum can build. Then, underwriting begins, and the financing does not support the deal as originally understood.

Key Insight A deal isn't real until it can be funded.

Failed financing does not just delay a closing. It can cost time, weaken leverage, create unnecessary exposure, and leave the seller trying to restart the process from a less favorable position. This is why deal structure matters more than many owners realize.

In this article, deal structure refers to financing structure specifically: the combination of cash flow, lender support, buyer strength, liquidity, and supporting terms that determines whether a transaction can actually close.

Why A High Offer Is Not The Same As A Financeable Deal

Buyer interest is the beginning of the process. It is not proof that the process will hold together. A practice can attract attention because the location is strong, the revenue looks appealing, or the opportunity fits what a buyer wants. That attention matters, but it does not validate the financing.

Price agreement is another stage that sellers often overread. A buyer says they are willing to pay a certain number, and that can feel like the hard part is done. In reality, that number is often based on early information and untested assumptions. It has not yet passed through lender review, debt-service analysis, or structural stress.

The moment a deal becomes real is later. It becomes real when a lender determines that the practice, the buyer, and the structure work together in a way that can be funded and sustained after closing.

That is where sellers most often get caught off guard. They see a buyer, a price, and signed paperwork moving forward. The lender sees an unfinished underwriting question:

Until those questions are answered well, what the seller has is not a closed path. It is a promising path that still has to be proven.

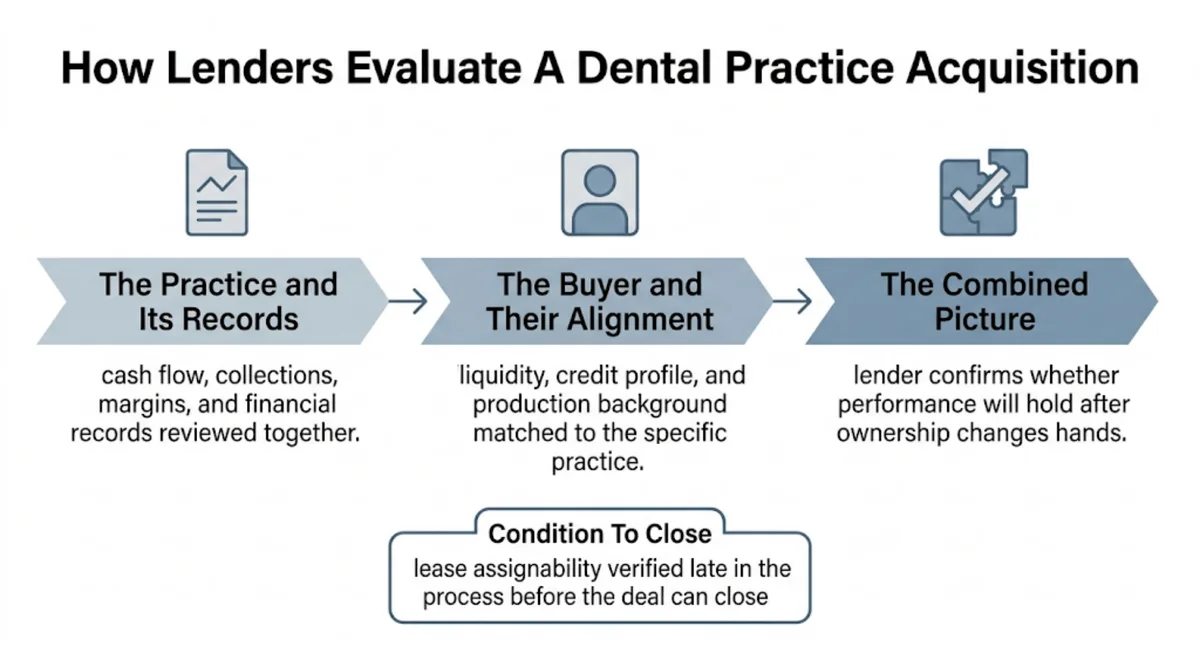

What Lenders Are Actually Underwriting In A Dental Practice Acquisition

Lenders are underwriting whether the business will remain stable and cash-flow-positive after the buyer takes over. They are not underwriting enthusiasm. They are not underwriting a headline valuation in isolation.

That review moves through three connected phases.

1 The Practice and Its Documentation

Lenders look at cash flow, collections, margins, and whether the business produces earnings that look durable rather than temporary. At the same time, they are reviewing whether the numbers hold across the full record: tax returns, profit and loss statements, and production reports all need to tell the same story. Lenders underwrite what they can verify, and uncertainty inside the records quickly becomes loan risk.

2 The Buyer

Does this buyer have the liquidity, debt profile, credit quality, and production background to step into ownership without becoming financially overextended? The lender is not just confirming that the buyer is qualified in general. They are verifying that this buyer fits this practice, that the transition is realistic given what the buyer has produced and what the practice requires.

3 Transition Durability

Once the practice and buyer pictures are established, the lender asks whether the combined picture holds. Is this practice likely to sustain its performance after ownership changes hands? That is not an operational question for its own sake. It is a repayment question.

One Additional Factor

One additional factor that must be resolved before a deal closes is the lease. Lease assignability and remaining term are not typically part of the formal underwriting review, but they are a condition to close. A deal can move well through underwriting and still face a late obstacle if the lease cannot be assigned cleanly or the remaining term creates concern.

Key Insight Underwriting is not a checklist. It is one integrated judgment about whether the acquisition remains financially sustainable after closing.

Why Financing Structure Changes What A Buyer Can Actually Pay For A Dental Practice

This is the part many sellers underestimate. Buyer willingness to pay and buyer ability to pay are not the same thing.

A buyer may genuinely want to pay a certain number. They may believe the practice is worth it. They may even offer aggressively because they do not want to lose the opportunity. None of that changes the monthly repayment reality that comes after closing.

That is where debt-service support becomes the decisive concept. Every practice has a practical ceiling on what it can comfortably bear financially. That ceiling is not set by excitement, and not always by appraisal alone. It is often set by what the lender believes the practice cash flow can realistically support month after month while still leaving room for payroll, rent, normal variability, and the buyer's own income.

This is why some valuation gaps are really financing gaps.

The seller may not be wrong about the quality of the practice. The problem may be that the current structure does not support financing at that level under a traditional lending model.

How This Plays Out

A seller agrees to a $950,000 price. The buyer is serious. An LOI is signed. Then the lender reviews the deal and concludes that, based on cash flow, the structure only supports something closer to $810,000.

What happens next depends on how the deal is being managed. In some cases, the bank simply moves forward at the lower number. The transaction closes at $810,000, and the seller loses $140,000 compared to what was agreed. This is not because anyone negotiated it away, but because the structuring was left to the bank, and the bank made its own determination. In other cases, the bank asks the seller to carry a note for the difference, turning the gap into a financing obligation the seller did not expect to take on.

When a seller note is introduced, the dynamic shifts further. The seller is no longer comparing offers but is being asked to absorb part of the financing weakness. The buyer, in turn, starts asking a different question: if the bank will not support this cleanly, is something wrong with the deal?

That is why seller financing has to be interpreted carefully. Sometimes it is a healthy bridge in an otherwise strong transaction. A modest seller note can help align buyer liquidity, lender comfort, and closing practicality. But when a seller note appears because the agreed price was never comfortably supportable in the first place, the note is not just a tool. It is a symptom.

Key Insight The highest theoretical price is not always the most financeable price. And the most financeable price is often the one that has the clearest path to actually closing.

What Makes A Dental Practice Deal More Or Less Bankable

Bankability is the practical expression of lender confidence. Lenders are looking for a deal that feels durable, verifiable, and financially manageable after closing.

✓ Stronger Bankability

- ✓ Strong and consistent cash flow

- ✓ Manageable overhead

- ✓ Clean reporting across all records

- ✓ Stable lease control

- ✓ A buyer profile that fits the practice

✗ Weaker Bankability

- ✗ Impressive revenue but thin cash flow underneath

- ✗ Stretched overhead

- ✗ Buyer with limited liquidity

- ✗ Uncertain lease control

- ✗ Structure depends on optimistic assumptions

One of the most common lender-facing issues is reporting quality. Sellers sometimes assume a good business will speak for itself even if the records are messy. It does not work that way. If tax returns do not align with internal reports, if add-backs are not clearly supported, or if numbers require too much explanation, lender confidence declines. In many cases, uncertainty itself becomes the risk.

The trailing P&L issue is a good example. Some sellers or advisors present trailing financials in a way that smooths over softer periods or makes earnings appear stronger than the historical picture would suggest. That may help the practice look better at first glance, but if the presentation does not reconcile cleanly with tax returns and other records, it creates the exact kind of hesitation lenders react to.

Bankability can also weaken through buyer communication, not just financials. A buyer may look qualified on paper and still create concern if, during underwriting, they sound uncertain about how they will sustain production or describe a post-close plan that does not fit how the practice actually runs. Lender confidence is partly a function of the buyer's confidence in the deal itself.

Bankability is not a separate label layered on top of the transaction. It is the lender's answer to whether the deal, as presented, holds together under real scrutiny.

How Sellers Misread Financing Strength In A Dental Practice Sale

Sellers usually misread deal strength in three ways.

First: High Revenue Automatically Means Strong Financeability

Revenue alone does not repay debt. Cash flow does. A high-collection practice with weak margins may still become difficult to finance comfortably.

Second: Buyer Interest Means Buyer Bankability

A buyer can be highly motivated, professionally credible, and genuinely committed, while still lacking the liquidity, debt profile, or financing fit the transaction requires.

Third: Valuation Tells Them What Will Fund Cleanly

Appraisal and closeability are related, not identical. A practice can appraise well and still require structural adjustments if the lender does not believe the deal works comfortably as proposed.

When sellers proceed on those assumptions, the consequences usually show up late.

Time and Lost Momentum

Financing problems tend to surface after conversations, diligence, and emotional investment are already deep.

Leverage

Once a deal weakens in underwriting, the seller is no longer negotiating from a fresh position. Questions increase. Confidence decreases.

Confidentiality Exposure

Every failed attempt usually means more document sharing, more conversations, and more people aware that the practice may be in play.

Process Fatigue

Sellers who go through a late-stage financing failure often become more willing to compromise just to get the next deal done.

A Harder Second Attempt

Even if the practice itself has not changed, the process now carries history.

This is why financing weakness rarely appears as one dramatic moment. More often it shows up as delay, reduced loan support, a request for seller carry, retrading, or a visible drop in buyer certainty. By the time those signs are obvious, the seller is already paying for the original misread.

The Real Question Sellers Should Ask About Deal Structure

When comparing offers, sellers tend to focus on price first. That is natural, but headline price is only one part of the decision. Fit still matters for transition success, but the practical question is which deal has the strongest path to actually closing.

That means comparing:

-

How comfortably the practice supports the debt

-

How strong the buyer is financially

-

How much strain the structure places on the transaction

-

How likely the lender is to support the deal cleanly

-

How much certainty exists between price agreement and closing

In many cases, the better deal is not the one with the highest headline number. It is the one where price realism, buyer strength, and lender support align without forcing the seller to absorb problems that should have been visible earlier.

The Bottom Line

Financing structure is often the invisible factor that determines whether a deal actually closes successfully, or slowly starts coming apart once underwriting begins.

For too long, many sellers have been asked to accept that process as normal: go to market, collect interest, sign paperwork, and then wait to see what financing says. Dental Shop is built to change that: giving sellers more visibility earlier into what the practice requires financially, what kind of buyer profile actually fits it, and what type of structure is likely to close cleanly.

Deal structure matters more than most owners realize. It does not just shape price on paper but also whether the deal is real at all.

Understand what your practice can support

Get a free, transaction-focused valuation — built to reflect what buyers and lenders actually evaluate, not just a headline number.

Value Your Practice

About the Author

Andrea Berk is an entrepreneur and business strategist specializing in dental practice growth, operations, and practice transitions. She is the Founder of The Dental Shop, where she works closely with dentists at every stage of their careers to help them make smarter decisions around buying, selling, scaling, and optimizing their practices. Andrea brings a practical, real-world perspective to complex business challenges facing dental professionals today. Her work focuses on helping practice owners increase efficiency, improve profitability, and build long-term enterprise value—without losing sight of patient care or work-life balance. Andrea regularly publishes insights on dental practice management, business strategy for dentists, practice transitions, and entrepreneurship, offering actionable guidance designed to help owners navigate growth with clarity and confidence. When she’s not advising practice owners, Andrea is focused on building scalable systems and partnerships that elevate independent dental practices nationwide.